Deciphering the Closing Disclosure: What Buyers Need to Verify Before Closing

It's Friday, and you've reached the final financial milestone of your home-buying journey. The inspections are complete, the appraisal has been approved, and your loan has successfully cleared underwriting. Now your lender is preparing one of the most important documents you'll review before becoming a homeowner—the Closing Disclosure (CD).

Under federal lending regulations, you must receive your Closing Disclosure at least three business days before signing your final loan documents. This review period gives you time to carefully examine the numbers, ask questions, and ensure everything matches the terms you agreed to throughout the transaction.

Here's what you should review before heading to the closing table.

Confirm Your Loan Terms

The first page of the Closing Disclosure outlines the key details of your mortgage. Take time to verify that the following information matches your expectations:

- Loan amount

- Interest rate

- Loan term

- Loan type (fixed-rate or adjustable-rate)

You'll also see your estimated monthly payment, including principal, interest, property taxes, homeowners insurance, mortgage insurance (if applicable), and any escrow payments.

Carefully reviewing these figures now can help prevent surprises after closing.

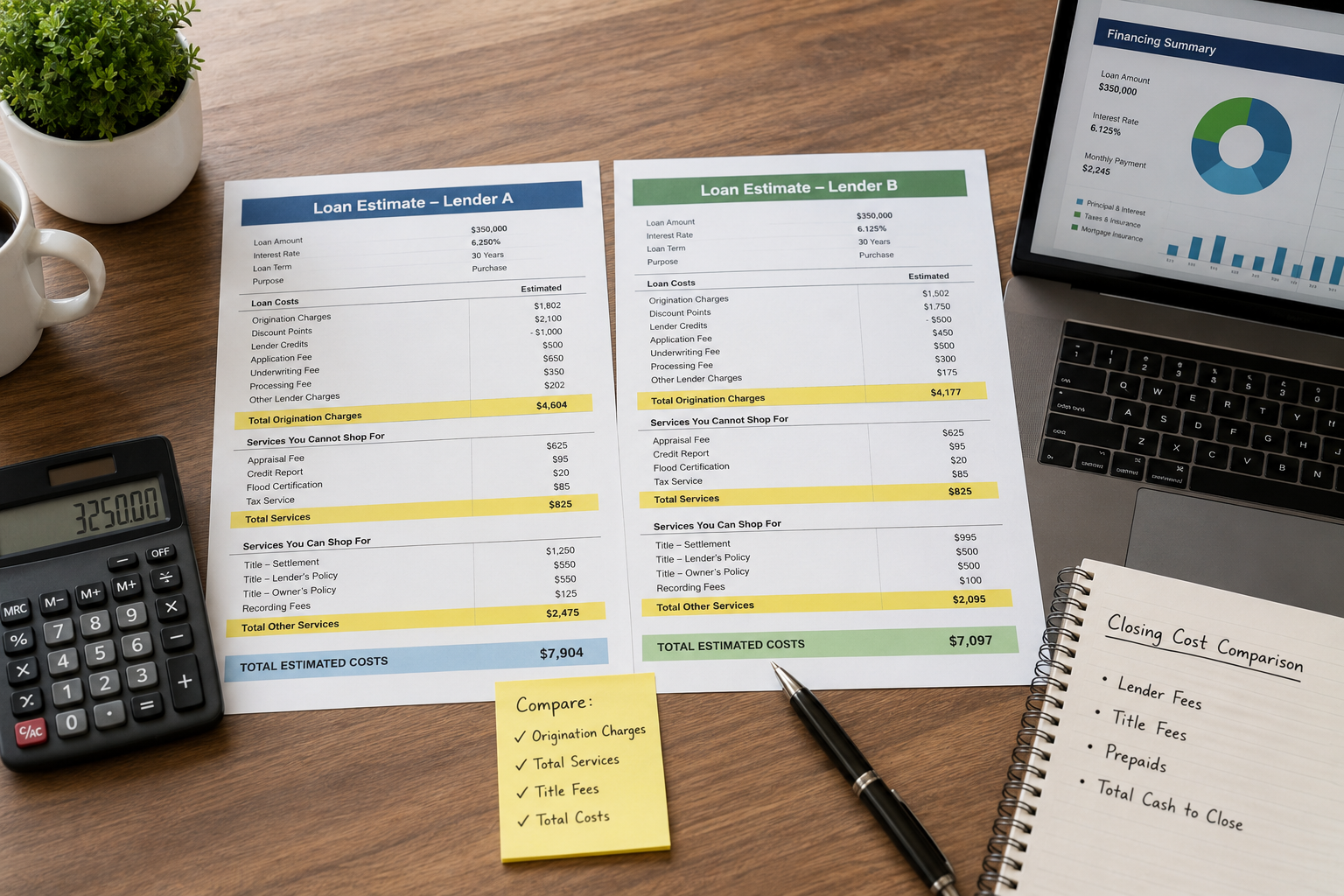

Compare the Closing Disclosure to Your Loan Estimate

One of the most valuable tools you have is your original Loan Estimate.

Your lender is required to keep many loan costs consistent between the initial estimate and the final Closing Disclosure. While certain third-party charges—such as prepaid taxes, insurance premiums, or recording fees—may change slightly, many lender-controlled fees should remain the same.

Pay particular attention to items such as:

- Loan origination charges

- Processing fees

- Underwriting fees

- Administrative lender costs

If you notice unexpected increases or unfamiliar charges, contact your lender immediately and ask for an explanation before signing.

Verify Your Cash to Close

The third page of the Closing Disclosure contains one of the most important numbers in the transaction: your Cash to Close.

This section provides a detailed breakdown of the funds you'll need to bring on closing day. It accounts for:

- Your earnest money deposit

- Down payment

- Seller concessions or credits

- Loan proceeds

- Closing costs

- Prepaid expenses

Review this calculation carefully so you'll know the exact amount to transfer by wire or obtain through a cashier's check before closing.

Review Your Escrow Account

If your mortgage includes an escrow account, the Closing Disclosure will explain how it's being established.

Most lenders collect several months of property taxes and homeowners insurance at closing to create an initial reserve. Verify that:

- Your homeowners insurance policy information is correct.

- Property tax estimates are accurate.

- Any applicable exemptions have been properly reflected.

- The escrow amounts align with your lender's requirements.

Understanding how your escrow account works now will help you manage your future monthly payments with confidence.

Ask Questions Before You Sign

The Closing Disclosure is designed to provide transparency—not confusion. If any number, fee, or loan term doesn't make sense, don't hesitate to ask for clarification.

Taking a few extra minutes to review the document carefully can provide peace of mind and help ensure your closing proceeds without unexpected surprises.

Ready for Closing Day?

Buying a home is one of the biggest financial decisions you'll ever make, and you shouldn't have to navigate the paperwork alone. I work closely with my clients, lenders, and local title professionals to review every detail before closing so you can move forward with confidence.

I'm Jason L. Jenkins, and I'm here to guide you through every step of the Albuquerque home-buying process. If you're preparing to purchase a home, contact me today and let's make your closing day a smooth and successful experience.

Categories

Recent Posts

"My job is to find and attract mastery-based agents to the office, protect the culture, and make sure everyone is happy! "